SMM News on May 14: Today, driven by positive policy developments, the main lithium carbonate futures contract showed an overall fluctuating upward trend after opening, surging over 3% at one point during the session. By the close of the daytime session, the main contract closed up 3% at 65,200 yuan/mt, rising 2,640 yuan/mt from the low of 62,560 yuan/mt set during the session on May 12, representing a 4.22% increase.

In terms of spot prices, according to SMM's spot quotes, the spot price of battery-grade lithium carbonate also rose slightly by 100 yuan/mt today, trading at 63,600-65,800 yuan/mt, with an average price of 64,700 yuan/mt.

》Click to view SMM's spot quotes for new energy products

Regarding the reasons for the rise in lithium carbonate futures prices, SMM believes it is mainly related to positive policy news. On May 12, the Ministry of Commerce website released a joint statement on the China-US Geneva Economic and Trade Talks, stating that the US's 24% reciprocal tariff on Chinese products would be suspended for the initial 90 days. According to the latest news today, this tariff adjustment has been temporarily implemented. SMM understands that, overall, due to exemptions for NEVs and their parts before and after this reciprocal tariff adjustment, the change in reciprocal tariffs will have a greater impact on the export of ESS batteries. This may drive expectations of a rush in exports of Chinese ESS battery cells, thereby boosting the demand for lithium carbonate.

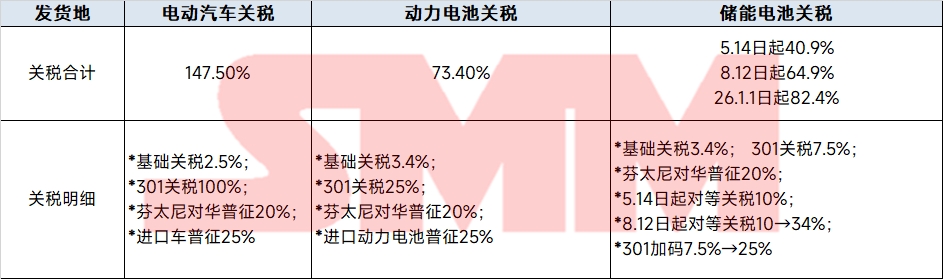

From May 14, the tariff on new energy end-use products exported from China to the US is as follows:

SMM predicts that, given the installation rush demand for ESS storage mentioned in China's Document No. 136 regarding the "May 31" grid connection deadline, the ESS battery cells produced in May may not be able to meet the installation rush demand in time this month. Therefore, the market previously expected that the production volume of ESS battery cells in May may decrease by 5-10% MoM compared to April. However, influenced by the golden export window period brought about by the change in US tariffs, and considering that it takes approximately one month for transportation and customs clearance from China to the US, it is expected that the production schedule of ESS battery cells for top-tier enterprises will remain at a high level in May and June, and the growth rate of ESS battery cell production is expected to turn from negative to positive MoM.》Click to view details

Returning to the supply and demand dynamics of the lithium carbonate market, lithium carbonate prices currently remain near recent lows. Under the pressure of cost losses, upstream lithium chemical plants have shown a strong sentiment to stand firm on quotes. Currently, there is only a certain level of trading activity between traders and downstream enterprises. The positive expectations for an increase in end-use demand driven by the aforementioned policy developments may, to a certain extent, drive a rebound in lithium carbonate prices. However, it should also be noted that although lithium carbonate inventory has slightly destocked after the Labour Day holiday, the current cumulative inventory level of lithium carbonate remains high. Additionally, ore prices continue to fall to new lows, with cost support continuously weakening. Therefore, the overall price of lithium carbonate will continue to exhibit a fluctuating trend at lows.

As the futures and spot prices of lithium carbonate rose together, the shares of energy metal companies, including Tengyuan Cobalt, Huayou Cobalt, YOUNGY, Zhongkuang Resources, Weiling Co., Ltd., and Tianqi Lithium, also "rose", with multiple stocks increasing by over 1%.

Dazhong Mining also responded today on the investor interaction platform regarding the progress of the lithium mine tunnel in Hunan. The company stated that as of now, the lithium mine tunnel in Hunan has been completed, laying a certain foundation for the early commissioning of mining and beneficiation operations. According to the "Lithium Exploration Report of the Tongtianmiao Ore Section in the Jijiaoshan Mining Area, Linwu County, Hunan Province" reviewed and filed by the company for its resource reserves, the associated minerals of the Jijiaoshan lithium mine in Hunan include metals such as rubidium, niobium, tantalum, tin, and tungsten.

Institutional Comments

Xinhu Futures commented that there are no obvious positive factors in the short-term fundamentals, making it difficult for lithium prices to reverse their trend. However, at the current price level, it is necessary to be vigilant about the rising expectations of supply-side disruptions and the capital-driven factors amid low valuations. Given the relatively high channel inventory levels across the upstream, midstream, and downstream sectors, the rebound space for lithium prices will also be limited.

Yide Futures stated that, on the supply side, the CIF price of Australian ore has fallen to $687.5/mt, while the price of African ore has remained stable at $637/mt. Port lithium ore inventory has increased, and the planned production of lithium carbonate nationwide for May has increased MoM, with the latest weekly production data showing a significant increase. On the demand side, the planned production of cathode materials, including ternary and LFP, has increased MoM. Based on the current production schedule, the supply and demand fundamentals still maintain a surplus pattern. In terms of inventory, the latest weekly inventory has decreased by 464 mt. Specifically, the significant increase in smelter production has not yet been transferred downstream or to traders, leading to a noticeable increase in their inventory, while the inventory of downstream traders has decreased. In the short term, the combination of front-loaded consumption and collapsing costs has led to a significant pullback in lithium carbonate prices. From a long-term industry perspective, the market requires a more thorough exit of resources.

SDIC Futures stated that the total market inventory has decreased by 500 mt to 132,000 mt, with downstream inventory decreasing by 3,000 mt to 42,000 mt and smelter inventory increasing by 3,800 mt to 55,000 mt. The intermediate links are actively destocking. In terms of inventory structure, there is a weak willingness for downstream restocking, while the upstream is experiencing passive restocking, reflecting differences in market sentiment. The latest quote for Australian ore is $700, with a decline of over 15% in the past month, basically reflecting a downward shift in the price center. The midstream production has recovered rapidly, with a 28% increase in production MoM in the first week after the holiday, and an improvement in supply and demand still needs to be awaited. The futures price of lithium carbonate is in a downward channel, and the holding of short positions continues.